No. of Recommendations: 19

But if the US stock market's returns continued to outpace other countries, as they've done for quite some time (past performance not predictive... you know the line), it could still be a net advantage to invest in the US even if a person hypothetically was subjected to the maximum 20% additional tax.

I haven't confirmed these numbers, but here's what AI says were the European stock market performances vs. S&P500 in the last 25 years:

S&P 500 (USA): ~7.5% CAGR

MSCI Europe Index: ~5.5% CAGR

Germany (DAX): ~6.0% CAGR

France (CAC 40): ~4.8% CAGR

UK (FTSE 100): ~4.0% CAGR

Other European Countries: ~3-5% (Limited data for smaller markets (e.g., Spain, Italy, Netherlands)

This doesn't consider valuation levels...I think that in this context it is very important--nay, dominant--to consider valuation levels. Because that's the entire reason that a US stock has risen in price more than a non-US stock.

Much of the rich world's equities could be divided into three buckets:

(a) A half dozen obscenely profitable US giants

(b) The rest of the US market

(c) European-listed equities

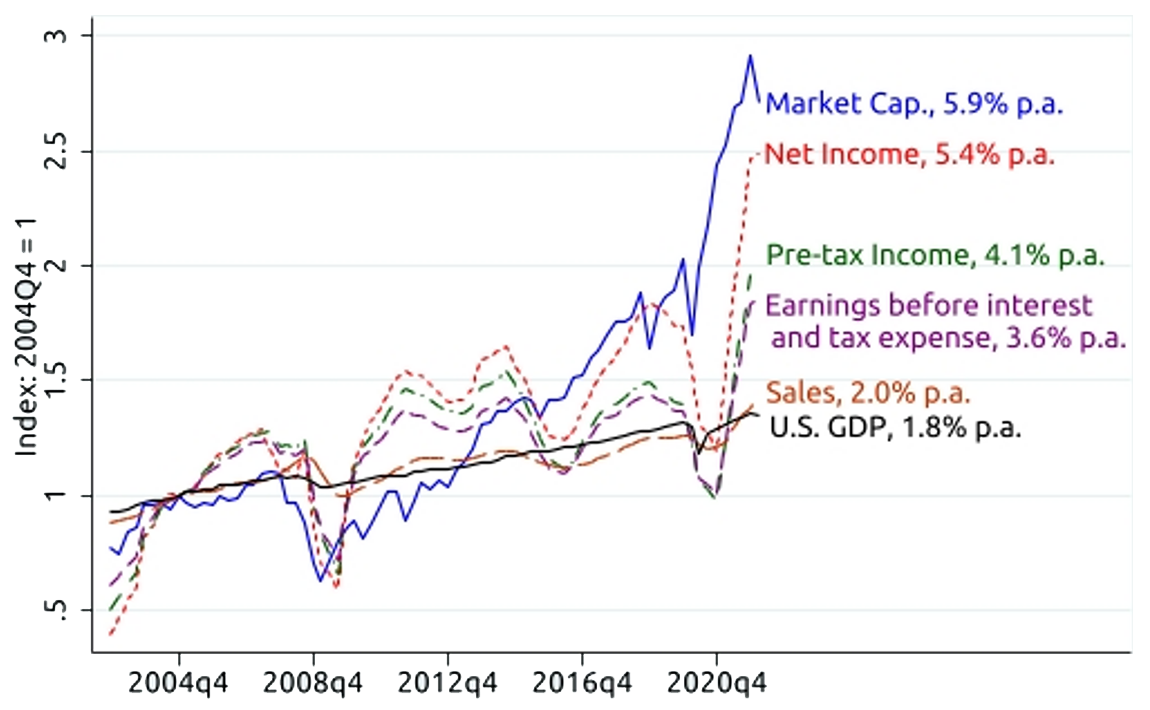

Obviously (a)+(b) taken together, the US broad market, have obviously delivered mark-to-market returns better than (c) for a long time.

Ignoring (a) for the moment, the interesting thing is that profits have grown faster in group (c) than in group (b). Surprise! Typical European firms have grown in value faster.

Again, ignoring a few wildly profitable firms like Alphabet, Meta, Apple and Microsoft, the market price outperformance of the US market in the last 30 years is entirely due to getting more expensive: rising valuation multiples. This trend is obviously not something you would want to extrapolate.

The US productivity miracle is mostly better thought of as the US bubble. Or secular bull market, if you prefer.

If you run a trend line through the CAEY earnings yields of the S&P 500 in the last 40 years, you see that about 1.58%/year of the S&P 500 total return in the last 40 years has been multiple expansion. That's based on reported earnings; you get a bigger number if you use sales to take out some of the one time run-up in net profit margins from lower interest and taxes in the last 10-15 years.

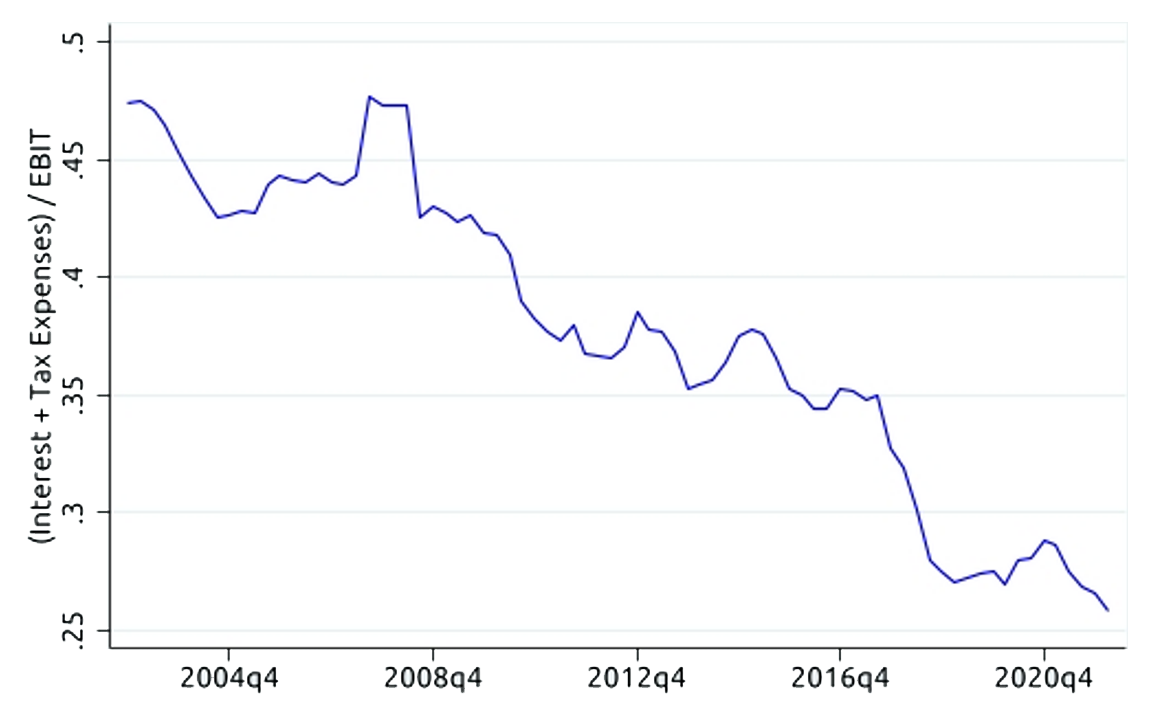

A pair of nice images from a Fed paper that makes the point visually, covering the stretch roughly 2002-2022

https://www.federalreserve.gov/econres/notes/feds-...https://www.federalreserve.gov/econres/notes/feds-...The last sentence of the paper from which those were cribbed:

"The overall conclusion, then, is that�with the expected slowdown profit growth and the associated contraction in P/E multiples�real longer-run stock returns are likely to be notably lower than in the past." In short, a cyclical factor on profitability combined with a cyclical factor on valuation multiples. I think the S&P 500 is up around 40% since that was written.

A completely different administration will be in office in over 3.5 more years.I admire your optimism! Not about the election outcome, but about the election happening. I have the working assumption that will not be any 2028 US election, merely an "election". As always, I hope to be pleasantly surprised.

Jim

{kind=link}

{kind=link}