It is as difficult to sink a business without debt as it is sink a ship without holes.

- Manlobbi

Halls of Shrewd'm / US Policy❤

No. of Recommendations: 0

'Warren Buffett is famous for his patient investment style, having said that his favorite holding period is 'forever.'

His Berkshire Hathaway (ticker: BRK/A, BRK/B), however, has been churning through equity holdings in recent years, including Verizon Communications (VZ) and a group of drug stocks. In fact, eight of the top 15 equity holdings listed in Buffett's 2019 annual shareholder letter are gone or much reduced.'

No. of Recommendations: 0

'Given the subsequent gains in many of the stocks that Berkshire unloaded, the company would have done better to keep them in its $350 billion equity portfolio.

The most notable recent example is Taiwan Semiconductor Manufacturing (TSM), or TSMC, according to Berkshire's latest 13-F filing.

In the third quarter, Berkshire bought a stake of 60 million Taiwan Semi shares, only to sell 86% of the holding in the fourth quarter to end 2022 with just 8.3 million shares, worth less than $800 million. The news of the stock sale, which occurred after the close of trading Tuesday, is dragging down Taiwan Semi stock, which slid 6.6% to $91.53 in recent Wednesday trading.

READ MORE

Charlie Munger Musings

Warren Buffett Runs Berkshire Hathaway Like It's the 1960s.

Berkshire might not have made any profit on the stock, given that the average price of Taiwan Semi averaged $72 a share in the fourth quarter, $10 less than in the third quarter. Berkshire has missed out on some nice gains so far in 2023, with TSMC up about 24% year to date. Berkshire's purchase of the stock generated a lot of excitement when it was disclosed in mid-November; Taiwan Semi stock popped more than 10% on the news. But this latest round of turnover suggests that investors may want to curb their enthusiasm about the disclosure of new Berkshire investments.'

No. of Recommendations: 0

' Berkshire didn't immediately respond to a request for comment on Wednesday.

Verizon stock was another holding that wasn't forever for Berkshire. After accumulating a $9 billion stake in Verizon Communications mostly in 2020, Berkshire eliminated it in the first half of 2022 and likely took a small loss.

Similarly, in late 2020, Berkshire bought roughly $2 billion stakes in each of three drug companies' Merck ( MRK ), Bristol Myers Squibb (BMY), and AbbVie (ABBV)'and those are gone now and are higher in price in the sales.

''

No. of Recommendations: 0

' Looking at the top 15 stocks listed in the 2019 annual letter published in February 2020, Delta Air Lines (DAL), Goldman Sachs Group (GS), JP Morgan Chase (JPM), Southwest Airlines (LUV), United Continental Holdings (UAL), and Wells Fargo (WFC) have been eliminated. Holdings of U.S. Bancorp (USB) and Bank of New York (BK) have been cut back significantly.

Buffett has sharply reduced Berkshire's bank-stock holdings and now is concentrated in a $36 billion investment in Bank of America (BAC). The bank-stock sales'especially Wells Fargo'weren't well-timed. Barron's estimates that Berkshire got roughly half of Wells Fargo's current price of $48 a share, for what had been a longtime stake of nearly 350 million shares. Overall, Barron's estimates that Berkshire has left more than $10 billion on the table with its bank-stock sales.

The airline stocks were sold after the onset of the pandemic in the second quarter of 2020 at prices below current levels.'

No. of Recommendations: 0

' Buffett told CNBC in early 2019 that he thought bank stocks were appealing because of low valuations. At the time, he singled out JPMorgan stock, then trading around $100'it's now at $143.

'A business that earns 15% or 16% or 17% on net tangible equity, that's incredible in a world of 3% bonds. I mean, just imagine that you had a deposit account with JPMorgan that they made a mistake and they gave you 15% on it. And they couldn't redeem it. What would you sell that account for? You wouldn't sell it for 100 cents on the dollar. You wouldn't sell it for 200 cents on the dollar. You wouldn't even sell it for 300 cents on the dollar,' he told CNBC at the time.

That analysis suggested that the bank should trade for three times tangible book'or about $150 at the time. That is roughly where the stock trades now, although the current price to tangible book value is two, one of the higher valuations among its peers. JPMorgan's book value is higher since then.

While there has been great churn in the portfolio, the largest Berkshire holdings have shown little or no change in the past few years, including Apple (AAPL), American Express (AXP), Bank of America, and Coca-Cola (KO).

Berkshire bought a $12 billion stake in Occidental Petroleum in 2022, which Barron's estimates has gained more than $2 billion. Buffett's company also greatly expanded its holding in Chevron (CVX) to nearly 170 million shares worth around $29 billion in 2022. That holding could have a gain of close to $9 billion.' Bary wrote this piece.

No. of Recommendations: 1

There are many interesting well reasoned comments to this story, most are not complimentary. This is too funny not to share, if you want the substantive comments just ask and I'll share more. '' Back before I retired from the business, if I had a 92 year old client increasing his level of trading this much I would have received a call from the Compliance Dept. inquiring about his mental condition.''. Lol.

No. of Recommendations: 10

hclasvegas

When I tune in to the board, I see six consecutive posts by you concerning Buffett's stock trades.

Could you summarize what point you're trying to make?

No. of Recommendations: 1

That's the only way I know how to share it without the ads etc. The point is, Buffett has some, explaining to do, no? You think that story is off topic?

No. of Recommendations: 8

The point is, Buffett has some, explaining to do, no? You think that story is off topic?

Not at all. I just want to be clear that I understand on what point Buffett has to explain.

I decided long ago that I either had to trust Buffett's judgment or not. I cannot control what he does.

But I do value insights on what judgments he's making. That's my question.

Should I continue to trust him or not? What do you think?

No. of Recommendations: 0

Well, since you asked, I'm certain Buffett should be disclosing which trades are his, with every filing, otherwise, retail investors are making investment decisions based on inaccurate information. The press , cnbc etc should not be spreading news , with respect to brk trades, that brk refuses to confirm. To be honest, I think Buffett is making this error in judgement, to try and help T and T catch up to or outperform spy, which they have struggled to do. I've been pounding the table for aggressive buybacks at, material discounts to IV, for over a decade, so I guess I'm biased. Buffett should rethink this disclosure and transparency issue, asap, imo. Good luck.

No. of Recommendations: 7

A while lot of posters on Berkshire forums spend a lot of time being upset with "Buffett" as to Berkshire's use and placement of capital. To some degree it defines the forums as much as, if not more, than any anything else. Again it has for the 25 plus years I have spend on these forums.

I've not ever much thought about the stock trades myself, but I do read others views. I'm far more interested in the overall businesses, the operating ones, the capital use there does grab my attention. I tend to approve highly of the decisions in this arena.

No. of Recommendations: 4

Thanks hclasvegas.

I'm not making judgments, just trying to understand the viewpoints of others.

I appreciate the efforts of those who share their thoughts on these message boards. I can either agree or disagree. But I do try to understand where they're coming from. I like people who care and share.

That's what I was driving at - clarity. Appreciate the response.

No. of Recommendations: 0

Jeezz I can't spell. "A whole lot..."

No. of Recommendations: 0

'' I'm far more interested in the overall businesses, the operating ones, the capital use there does grab my attention. ''. Is , short term trading, included in, use of capital? Thanks.

No. of Recommendations: 4

No. But given it is a business it would not surprise me if quick decisons were multi-faceted and not necessarily related to what you as an individual investor may logically consider.

No. of Recommendations: 0

Tex, my pleasure, now I'll ask you a question? Why do you think Buffett refuses to disclose which trades are his quarterly? Do you think he is deliberately, deceiving ,the markets by allowing others to believe all these trades are his, in view of how the stocks react to the news, aka , misinformation? Thanks.

No. of Recommendations: 0

Dealraker, why force the markets to play, name that tune, every quarter? Buffett doesn't trade that often, disclose, his trades, and stop the games,imo.

No. of Recommendations: 18

hclasvegas

Do you think he is deliberately, deceiving ,the markets by allowing others to believe all these trades are his, in view of how the stocks react to the news, aka , misinformation? Thanks.

An emphatic NO. I don't think WEB cares to deceive anyone. Why should he?

If you're that interested, in past years I did try to look at who did the investments. In the 13-f's, if I were paying attention, there was a column that indicated who was involved. Most of them involved only WEB. IF it involved others, you could tell. That basically answered the question about who was involved. I think most people on Wall Street understood that long before I did.

Since this has not been a concern of mine for some years, I'll leave it to current students of the 13-f publications to see if this is still available.

With time, these levels of detail have become much less important to me. Do T&T investments really impact BRK - or just those trying to follow them? Or Buffett.

I doubt it's changed. You just have to pay close attention.

Basically, I can make only one of four decisions about BRK. Buy, Sell, Hold, or Sell a little for living expenses. Those are the only decisions I focus on now. Other posters now provide a lot of the details I used to chase for myself about IV and such to make such decisions. So I've stopped. Frankly, I don't think it's that hard to do.

Book plus Float still works for me, although I pay attention to what others so generously share. It's an old correlation, but it changes only slowly. I think that's because it includes a number of factors that offset each other. Old acquisitions are understated, but new ones are at 1.0 book and don't change that fast. even sometimes in a negative fashion. Cash is 1.0 book. Equities are at 1.0 book with some fairly small adjustments for deferred taxes. More cash held for downsides, so less for investment impacting float value. More competition keeps prices more in line. Owned businesses don't change that quickly. On and on. If you back out the 1.0 segments, the others don't seem that far out of line. The big regulated businesses are easy to cross check versus competitors.

Many variables, but still only impact the above four decisions. Not that hard to judge. And those judgments don't happen that often.

Given that, I no longer find it a good use of my time.

Or worry about being deceived by WEB.

No. of Recommendations: 9

I'm not sure why Warren should need to explain which trades are his and which are T&T. Anyone piggybacking on these buys and sells knows ahead of time that it could be either. Neither Warren nor T&T invest for the sake of people who piggyback on their trades. They're running a holding company here. Either buy the stock if you like what you see or don't. And certainly sell it if you're not comfortable with the amount of disclosure or strongly disagree with the moves being made. There are so many options out there for investing your money.

If anyone isn't sleeping soundly, then you should re-evaluate your portfolio and get it in line with what allows you to get your needed rest. I think we can all agree on that.

best wishes to all,

SD

No. of Recommendations: 0

You don't think it's material that the financial press is consistently misreporting that brk trades are Buffetts , when they aren't? When it's disclosed that Buffett bought a stock, does it tend to trade up 2-4 percent? When it's disclosed that Buffett sold a stock, does it tend to trade down 2/4 percent? Do t and t have an , edge, if their buys are goosed 2-4 percent, because the financial press reports the buys, as Buffett buys??

No. of Recommendations: 0

Tex, 13 f and G filings disclose if Buffett was the buyer or seller?

No. of Recommendations: 17

If Warren were to pay attention and respond to press reports, he'd spend too much time managing them and not the business. The press are going to do what they're going to do. It's not Warren's job to do their job for them. Anyone foolish enough to copy moves made by another investor without doing their own due diligence deserves whatever happens. It's not Warren's fault. It's statistical noise. You can't control the press. If you try to coddle them, they'll just want more coddling. Tough love. No comment. Ever.

No. of Recommendations: 17

Changing one's mind over a recently established 1% position hardly qualifies as rapidly churning the portfolio.

Buffet's role is a capital allocator for the entire business not a stock trader who has to report his quarterly buys and sells to the gallery.

No. of Recommendations: 3

Smurf's response is it. Perfect summarization.

No. of Recommendations: 0

Good morning all. What would Buffett and Munger say? What would rational walk, the Brooklyn investor or Jim say? Why does Buffett often request permission from the SEC to delay reporting his trades? He knows there is a Buffett bounce and he doesn't want to have to pay up to complete his trade. If T and T were going to challenge another money manager to a performance test, short term, would T and T have an edge, if their buys were reported as, Buffetts buys ? Why did Buffett agree to create the Bs? The lack of transparency causes confusion every quarter and benefits t and t if they continue to make short term trades. This issue is complicated or controversial? Suggesting brk should split the Bs 50 for 1, was controversial, until they did it. Suggesting brk should authorize buybacks at, material discounts to IV, was controversial ,until they did it. Within two years, maybe sooner, brk will disclose in a timely manner, which trades are Buffetts. I'm sure honorable guys like T and T would agree. Have a great day all.

No. of Recommendations: 14

why force the markets to play, name that tune, every quarter?

Buffett has stated quite clearly that he does not want to disclose more about his trades than the law requires, for strategic reasons. He has however given us a bit more information than he needed to - he has said that small trades will almost always be from one of his lieutenants (T&T), although the recently increased size of their portfolios makes some ambiguity possible.

Of course we are curious and we speculate about who has done what trade, and why positions recently opened have been closed, and why there is sometimes some trimming of positions or tiny increases. No one is forcing us to play this game, but no one is stopping us from playing either. Let the game go on, but please, no whining!

DTB

No. of Recommendations: 8

"Buffett has stated quite clearly that he does not want to disclose more about his trades than the law requires, for strategic reasons. He has however given us a bit more information than he needed to - he has said that small trades will almost always be from one of his lieutenants (T&T), although the recently increased size of their portfolios makes some ambiguity possible."

Notice how this extra information beyond the legal floor is strategically beneficial for BRK, and thus for BRK shareholders. If it's a small trade (Buffett says, and the market mostly listens) assume it is T & T. Ergo, no Buffett bounce for small new positions.

That is, the extra disclosure provides BRK, including Buffett & T & T, the leeway to buy small & add without a Buffett-induced market headwind.

In any case, I have more than enough disclosure to know where BRK's money goes, what they hold, what their liabilities are, and the like. I have no interest in BRK compelling disclosure re: operations, above and beyond the legal floor, if it is to their disadvantage.

So, my own view: absolutely not, I do not want Buffett et al. tipping their hand more than is legally required and/or strategically useful. And when the time comes to assess BRK as a Buffett-less enterprise, I'll continue to assess the ins and outs of BRK as a whole.

No. of Recommendations: 19

Tex, 13 f and G filings disclose if Buffett was the buyer or seller?

I haven't looked at a 13F official form in decades. So the reporting details may well have changed. People race each other to publish and analyze changes. And others point out what isn't reported.

Back in my prime years I was interested in somewhat the same info you're seeking. In my case I was trying to separate out the stocks in Lou Simpson's portfolio.

Going on distant memory, there was a column that indicated who had sole power to buy and sell that particular listing and where that power was shared. When it was shared, they indicated who else had that power. By sorting through a lot of details, I could pretty well identify the Simpson stocks.

I quit doing it because (a) it took effort and (b) I quit caring about this level of detail. I had realized that I wasn't going to try to let their actions dictate my buys and sells. I was just being nosey. I wasn't chasing stock tips.

Buffett used to say that the annual reports included all the info he thought was important in making decisions on BRK stock. I tracked financial data by quarter on a per share basis, plotted it, did the statistics, etc. I finally latched on to what I had been told was the Gottesman criteria from the early days. Track the sum of float plus book value. When the price was significantly below that sum, buy. When I looked at the graphs, the good opportunities to buy and sell stuck out like a sore thumb. It wasn't hard to guess where the current quarter stood, you didn't have to be that close. The long term correlation of the ratio of B+F to price was close to 100%. So you were looking for some significant departure from that correlation. Ignore the noise.

Things have changed in business structure, cash reserves, a lot of stuff. So this should be less useful now than it used to be. But it surprisingly remains a pretty tight correlation. I think, as said earlier, that there's a number of items that tend to offset each other so that the change - just like P/B - takes place slowly.

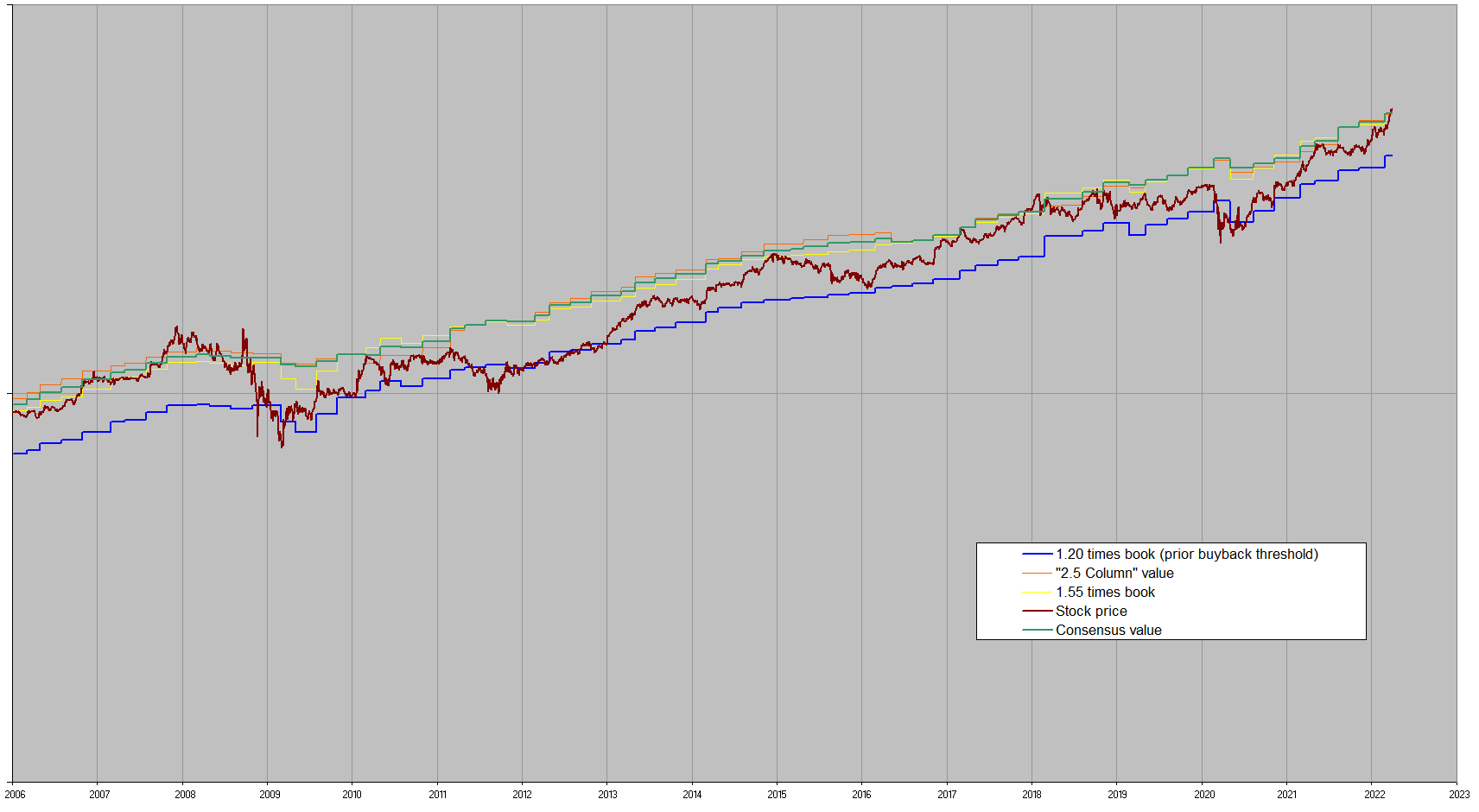

I personally like Jim's 2.5 column best, and appreciate what he shares. It's sensible. P/B is still useful. I understand WEB's points, but that's going to be a lengthy process. There are followers of BRK who publish their detailed estimate of sum of the parts - with a significant spread in their estimates. I watch them all - I'm still a BRKaholic. But I think people may overwork analyzing BRK unless they're doing much more sophisticated investing than I'm doing - options, etc.

I admire their work and thank them for sharing. But it's not for me.

What is important to me is to try to identify events that might have a major impact on BRK going forward. And I'm not talking about succession. That's where I'm trying to spend my reading and thinking time. And keeping in touch with some very smart long term BRK investors who think along similar lines.

No. of Recommendations: 8

I don't know, this is a business that spits out a copious amount of cash every quarter to reinvest. I own other stocks that I worry daily about how their cash is being allocated. When it comes to Berkshire I just don't even bother worrying. That's not to say I'm not interested, of course I am, but what is the purpose of worrying about how all this is being reinvested when we've already created such an incredible profit stream? Mistakes will be made-- as in any business-- but far be it me to try and poke holes in what Warren, Charlie and the gang do. And to be fair I appreciate the comments to the contrary, they offer a valuable perspective that permeates our beloved Berkshire bubble but it just doesn't worry me what they are going to do with our money.

No. of Recommendations: 16

Like Tex,

"My Name is Ciao and I'm a BRKaholic" and probably spend way too much time on all things Berkshire but it keeps me entertained and forces reevaluation of what I think I know.

Like many here, BRK represents a major part of the family estate & will likely get passed on to the children & grandchildren.

Of all the valuations that are frequently discussed , I personally prefer the range of estimates provided by Jim in the past and frequently stare at the plot provided in a past post last updated in Q1 of last yr.

http://www.stonewellfunds.com/BuybackChart2022.pnghttp://www.datahelper.com/mi/search.phtml?nofool=y...A very infrequent check of the plot alerts me to either add some LEAPS when approaching the lower valuation or lighten up when approaching the higher valuation. This results in very infrequent trades and very satisfactory results ......leaving lots of time to "kibbutz" here at the BRK Coffee Shop in The Aether.

ciao

No. of Recommendations: 2

Good morning everyone, with a special thanks to those who participated in this discussion. Bottom line, if Buffett and Munger are going to pound the table for total transparency from others, see the crypto space etc, it's hypocritical to refuse to disclose which trades are Buffetts with every quarterly filing. Posting on these message boards has been a very interesting 20 year journey. It started on the yahoo board, then moved to the Fools board, but not much changed regardless of which Brkville madrassa we are on. Questioning Father Buffett on any issue always resulted in negative responses, 100 percent of the time. No one agreed that the Bs should be split 50 for 1, not one poster. No one agreed that buybacks should be authorized at, material discounts to IV no one. The Fools board had many sharp substantive posters back in 2010, yet, not one poster agreed with my suggestions. Now, it's the issue of transparency and disclosure. Not one member of the Brkville congregation can agree that munger and Buffett are being hypocrites, demanding transparency from others, while allowing the financial press to consistently mis report trading activity at brk. The good news is, Manlobbi is the new, cop on the beat, in this new and improved Brk house of worship, hence, I doubt he will block me, cancel me, take away from posting privileges etc, but, if he wants me to go away , no problem, I will respect his wishes. Btw, if Manlobbi or anyone else would like to see the messages I received from idiots on the yahoo and fools boards, just ask, I'll be happy to share them. Anyway, I have no doubt brk will in fact agree with my request soon enough. For the sake of disclosure , I'm currently about 20 percent long brkb but I'm also short the brk puts and the calls, which is little exposure relative to the past 25 years. Good luck to all, this has been another interesting experiment , thanks to those who joined in.

No. of Recommendations: 7

"You don't think it's material that the financial press is consistently misreporting that brk trades are Buffetts , when they aren't?"

It is the financial press misreporting the BRK trades, not Buffett. Why is he responsible for what the financial press says?

Buffett can't live his life going around trying to correct misreportings all of the time. If he did, he would literally not have any time to do anything else in his life.

Besides, because of stock liquidity issues, Buffett has always wanted secrecy in his trading.

"When it's disclosed that Buffett bought a stock, does it tend to trade up 2-4 percent? When it's disclosed that Buffett sold a stock, does it tend to trade down 2/4 percent? Do t and t have an , edge, if their buys are goosed 2-4 percent, because the financial press reports the buys, as Buffett buys??"

I think it would become quickly apparent to Buffett if T & T were trading on Buffett's reputation to goose their returns. I sincerely doubt he would find that acceptable and would quickly put a stop to it if he found it happening.

No. of Recommendations: 15

Posting on these message boards has been a very interesting 20 year journey. It started on the yahoo board, then moved to the Fools board, but not much changed regardless of which Brkville madrassa we are on. Questioning Father Buffett on any issue always resulted in negative responses, 100 percent of the time.

With that track record, maybe it's time to reconsider your positions. 20 years and 3 different boards cover a lot of time and people.

In the particular issue you're focusing on now, perhaps Buffett has other reasons for how Berkshire reports stock purchases and sales that have nothing to do with being a hypocrite. Many people have tried to gently point that out. Maybe its time to listen and consider their points.

I know that can be hard. In Dallas, it has been 25 years since the Dallas Cowboys have even played in a championship league game, must less won one. The one consistent factor is that Jerry Jones insists on being the general manager as well as the owner. As an owner, he's considered a marketing and management genius and has been elected to the NFL Hall of Fame. So it has nothing to do with his overall capabilities. He's just not a good judge of football talent, and won't accept that. And people have been pointing that out to him for a similar 20+ years. For a long time he was just stubbornly determined to prove he's right and everyone else is wrong. What he has done more recently is bring in an advisor that can judge talent. The drafts have gotten much better and we're getting closer (I hope.)

And you're not the only one who has ever critiqued Buffett. I've heard many doing so on his past refusals to do buybacks. He showed he could change positions.

Even earlier, before the shock of the sudden death of his first wife, I and others were critical of the lack of details and depth in his succession planning and what to do with his stock control of Berkshire. At the time, the successor was only known by a letter in his desk, and all of his stock was going to his wife. She's was a very nice person but also very liberal and not widely qualified. It took the shock of his wife's death to make him reconsider these factors. What has resulted is in depth succession planning involving the BRK board and teaming up with the Gates Foundation to more wisely utilize the bulk of his stock.

Maybe there are lessons to be learned from Jones and Buffett.

No. of Recommendations: 4

Could the sale of the bank stocks be a conscious effort to shift from dividend paying bond alternatives in a low interest rate environment to actual bonds in the current context of rising rates? Seems like he's trading equity risk for guaranteed returns at the same or slightly better coupon rates.

PhoolishPhilip

No. of Recommendations: 1

No. of Recommendations: 38

"Posting on these message boards has been a very interesting 20 year journey. It started on the yahoo board, then moved to the Fools board, but not much changed regardless of which Brkville madrassa we are on. Questioning Father Buffett on any issue always resulted in negative responses, 100 percent of the time."

It has been my experience (over 20 years of message board posting) that I always find that people who sarcastically say things like "Brkville madrassa" and "Father Buffett" aren't really open to understanding differing opinions.

It is just an easy, weak, and lazy way to dismiss anyone who views something differently without needing to understand.

From reading your posts from the past, I know you can be better than this. Now if you either refuse or are unable to understand why people disagree with you that is fine. And if you just then want to insult everyone who disagrees with you by implying they are unthinking idealogues, that is fine as well. Just realize that it reflects more on you than it does them. People here have made good faith arguments about why they disagree with you. You have ignored those arguments completely. Again that is fine, just realize that it is your loss, not theirs.

"Not one member of the Brkville congregation can agree that munger and Buffett are being hypocrites, demanding transparency from others, while allowing the financial press to consistently mis report trading activity at brk."

The reason no one will agree is because no one else thinks they are being hypocrites.

By calling Buffett a hypocrite over transparency, you are making the false argument that you are talking about the same type of transparency in multiple different situations. For one, Buffett has never called for "total transparency" from others. That is you making up something he has never said. Whenever he talks about transparency in others he is always talking about a specific type of transparency. What is total transparency anyway? For two, the transparency Buffett has been calling for in the crypto space is in no way related to the transparency of who buys what in Berkshire.

Your calls of hypocrisy would be more appropriate if Buffett has called out mutual funds (or other entities that could have multiple people making trading decisions) for not identifying the actual person who has made specific trade decisions. Except Buffett has never actually done that, so your hypocrisy charge is false.

The main reason your argument is false is because you use the word transparency in such a wide manner as to make it absurd.

You said "Bottom line, if Buffett and Munger are going to pound the table for total transparency from others, see the crypto space etc, it's hypocritical to refuse to disclose which trades are Buffetts with every quarterly filing."

Then you could easily argue:

Bottom line, if Buffett and Munger are going to pound the table for total transparency from others, see the crypto space etc, it's hypocritical for Buffett to refuse to publish a transcript of Berkshire board meeting minutes.

Or you could easily argue:

Bottom line, if Buffett and Munger are going to pound the table for total transparency from others, see the crypto space etc, it's hypocritical for Buffett to refuse to publish detailed transcripts of conversations he has with Tedd and Todd about potential trades.

Or you could easily argue:

Bottom line, if Buffett and Munger are going to pound the table for total transparency from others, see the crypto space etc, it's hypocritical to refuse to disclose which companies Buffett is talking to about potential acquisitions.

You will probably say those examples are absurd (and they are), but they are no less absurd than what you are demanding. The point is, just because Buffett has called for greater transparency in certain situations doesn't mean he has to tell you anything and everything you want to know about him and what he does regardless of the topic.

No. of Recommendations: 1

Umm, good morning , partner, and thanks for proving my point. Show me where I ever said or implied thus, ''The point is, just because Buffett has called for greater transparency in certain situations doesn't mean he has to tell you anything and everything you want to know about him and what he does regardless of the topic.''. You, are being a loyal enabler , and making it up as you go along. First, I'll remind you that no one has posted more love, respect, and gratitude to Buffett and Munger than me. For over 30 years they worked worked for us virtually free. No options, no free stock, no real cash compensation, that's why I own the stock for over 20 years. Presumably once B and M pass, TandT will be managing 30,40,50 billion of partners money, our money. Therefore, to celebrate their ten years with brk, I have an obvious question, how have they done? What's their average holding period? How many short term trades have they made? Knowing Buffett , my guess is he's bringing kind, and non confrontational, because that's who he is. I have no further interest in their opinion of crypto , who Buffett is doing due dili on, where they are exploring for potential use of capital, or their love life, follow? I'm asking a specific question, and you are running wild with the question, par for the course, for brk loyalists. Despite being beneficiaries of the Buffett bounce, I have a hunch the ten year performance of tandt has not been kind. I'm sure they are hard working, brilliant , honest guys, but I suspect Buffett has been proven correct, again. Even with an edge, it's very hard to beat spy over ten year periods. Have a grand day.

No. of Recommendations: 4

1. You want to know what the specific performance of Todd and Ted has been over the past 10 years?

2. You assert their performance has benefited from the "Buffett bounce", but is still less than the SPY over this period, correct? To quote, the performance "...has not been kind."

3. "No one has posted more love, respect and gratitude to Buffett and Munger than me."

Respectfully, given #3 above, I might suggest you reach out directly and don't be surprised if you receive a response that provides the information you seek. Then again, you might not - at which point you may have to make a decision (or several, I suppose).

I'm not sure why "average holding period" and/or "short term trades" are relevant, but I will admit to some small level of curiosity as to their overall performance. However, what is most concerning to me is the performance of the firm. Which I'm satisfied with since my first purchase, and every additional one.

Cheers!

ps. funny story (at least i think it is). new guy walks into one of our meetings and when it's his turn to share, he looks around the room and announces he could confidently say that he could drink each and everyone of us under the table. I suppose it could be true, but the bold audacity of it sure kept us laughing for a few days.

No. of Recommendations: 1

Hi, thanks for your reply. Holding period is relevant because if their average hold is five years, the Buffett bounce isn't that big of an edge. However, if they are generating many short term trades , the Buffett bounce might add 2 percent or so depending on how much misinformation is being reported, due to the lack of transparency. Btw, I don't drink 😇, but I love, your story. The audacity that anyone would question Buffetts thinking is, blasphemy,in Brkville, trust me , I know. However, I got my 50 for 1 split, I got my buybacks, and who knows, perhaps this year someone will ask Buffett what I consider to be a very material question. Take care partner.

No. of Recommendations: 12

I miss the old days when HC would demand that Berkshire pay a dividend

because, "strippers don't accept intrinsic value!"

Ah, good times!

No. of Recommendations: 8

"Umm, good morning , partner, and thanks for proving my point."

Good morning to you. Unfortunately I did not prove your point. You just misunderstood (yet again) what your opponents are saying and arguing. If you are just going to take the lazy way out and dismiss it as "loyal enabler and brk loyalists" rather than try and actually understand it that is fine. That is your loss, not mine.

I hope you have a good day.

No. of Recommendations: 0

Genius, keep it in context bud. Who were the experts who were calculating their, iv net worth, weekly? I tried to explain banks and brokers don't use iv net worth as collateral. Buffett had to increase demand for the common via a stock split and authorized buyback. In jest while chatting with Todd finance , beach lawyer etc, I explained that Vegas casinos and topless bars don't accept iv net worth checks either. The good old days. 🍿

No. of Recommendations: 13

regardless of which Brkville madrassa we are on. Questioning Father Buffett on any issue always resulted in negative responses, 100 percent of the time.

You are simply incorrect. Many many times we have had thoughtful discussions questioning WEB's actions. What brings about negative responses are condescending terms such as the string of metaphors and insults in your post.

No. of Recommendations: 17

Buffett had to increase demand for the common via a stock split and authorized buyback.

Sorry Manlobbi, I'm going to have to break the "no frowny face" string on this great new board.

The statement above is so far from fact that it makes any other of the author's viewpoints pale by comparison.

I'm no longer willing to waste time reading such rubbish.

Tex

No. of Recommendations: 11

"Buffett had to increase demand for the common via a stock split and authorized buyback."

If memory serves, the B shares were established at 50:1 during the BNSF acquisition. I believe it enabled BNSF employees (and shareholders) to participate more fully as owners on the other side of the deal. I happened to own both Brk & BNSF prior to the deal. In the immediate, the deal was very good for me as a BNSF shareholder. Over the longer term, the deal was great for me as a Brk shareholder.

It did increase my demand for "the common", but it wasn't the split so much as WEB's identification of a major & appreciating asset with public utility-like centrality to NA commerce. The pairing of BNSF with Brk's float was not something I fully appreciated at the time - colloquially known as "the frosting".

No. of Recommendations: 1

Do you really not know why there was a 50 for 1 stock split?

No. of Recommendations: 0

Hi, remind us, was an all cash deal off the table and not an option? The 50 for 1 may have facilitated getting the deal done, but, the added liquidity made brkb illegible for index inclusion as well.

No. of Recommendations: 10

This from a past 2017 Motley Fool article, re splits:

https://www.fool.com/investing/2017/06/01/5-key-mo..."3. Reaching out to small investors with Class B shares

In 1996, Berkshire Hathaway created its Class B shares, giving the right to existing Class A shareholders to convert each share of Class A stock into 30 shares of Class B stock at will. The net impact was to give small investors a way to invest in Berkshire, which at the time commanded more than $30,000 per Class A share.

Buffett didn't want to make the move, but he did so in response to financial entrepreneurs who sought to create an alternative investment vehicle to make Berkshire accessible to those with modest amounts of capital. Rather than allowing outsiders to reap fees, Buffett instead made the move himself, potentially saving ordinary investors thousands of dollars in added costs over the years and creating a way for them to participate in Berkshire's amazing run.

4. Berkshire's one stock split

Similarly, Buffett was never a fan of stock splits, but exigent circumstances did make one prudent. In 2010, Berkshire did a 50-for-1 split of its Class B stock. That made the shares more accessible to shareholders in railroad giant Burlington Northern when Berkshire bought out the company. The move allowed more Burlington shareholders to retain interests in Berkshire stock rather than having to liquidate what would have been fractional shares. Now, Class A shares are convertible to 1,500 Class B shares, and the current Class B price around $165 per share is squarely within the range of where typical stocks in the market trade."

ciao

No. of Recommendations: 1

<Under the terms of Tuesday's deal, Berkshire will pay about $100 for each Burlington Northern share, a price comprised of about 60 percent in cash and 40 percent in stock.

....

As part of the deal, Berkshire will split its class B shares 50-to-1 to help pay for the acquisition. It is an unusual move for Mr. Buffett, who has long said he did not like stock splits. Most of the stock component in the deal, however, will be in Berkshire class A shares.

>

https://archive.nytimes.com/dealbook.nytimes.com/2...

No. of Recommendations: 3

Things have changed in business structure, cash reserves, a lot of stuff. So this should be less useful now than it used to be. But it surprisingly remains a pretty tight correlation. I think, as said earlier, that there's a number of items that tend to offset each other so that the change - just like P/B - takes place slowly.

This is it. It's years now (15?) since I was reading valuations of BRK on fool.com and understood that book value was gradually getting worse and worse as an indicator, and "fair value" as price-to-book should be rising gradually over the years. I decided that ~1.75 was a fair level, even though ~1.5 was a more typical valuation.

So here we are years and years later, and price/book hasn't even got above 1.5 much. We now have probable buybacks below 1.2 (say) and 1.5 has been close to as high as it gets - this is a ridiculously small range for a single stock, I normally consider that any stock can double or halve in value, and the volatile ones do much more. So we have relatively low volatility, relatively underpriced which gives us higher annual growth and extra upside rather than downside, and all in a diversified, AAA company. Luxury!

(Are there other AAA companies worth considering? I seem to remember people saying there are hardly any left - perhaps that scarcity makes them more valuable?)

SA

No. of Recommendations: 4

and all in a diversified, AAA company. Luxury!

(Are there other AAA companies worth considering? I seem to remember people saying there are hardly any left - perhaps that scarcity makes them more valuable?)

There are so few left that Berkshire is no longer one of them. Alas, we are a lowly "AA"

Even the printing press possessing US Government is down to a measly AA+

No. of Recommendations: 31

It's years now (15?) since I was reading valuations of BRK on fool.com and understood that book value was gradually getting worse and worse as an indicator...

I think a more delicate wording would be this:

As time goes on, there is less and less reason to believe that book per share should remain a meaningful yardstick.

This remains a true observation.

However, more or less entirely by coincidence, so far it's about as good a yardstick as ever.

Even if you use a very fancy valuation method, you still get a number that rises at around the same rate and by the same overall amount.

(certainly within the error bars of any such valuation method, anyway)

This is because the big moving parts that drive down fair P/B, and the ones that drive up fair P/B, have roughly balanced.

There is no reason to assume that this balance will continue. But so far, all the fancy valuation work I've done has been a waste of time.

Except to the extent that, had I not done it, I wouldn't KNOW it had been a waste of time.

The main thing about book as a metric: I think it's fair to assume that future dips in book, like past dips in book, will all be transient.

By extension, when book drops a bit it's most sensible to assume that value hasn't dropped.

I can't think of any plausible way to come to the conclusion that a share isn't in reality worth *more* than it was a couple/few quarters ago.

Cash stacks up at around a billion per fortnight, for one thing.

We certainly haven't had any permanent value impairments of that magnitude.

Jim

No. of Recommendations: 8

<<(Are there other AAA companies worth considering? I seem to remember people saying there are hardly any left - perhaps that scarcity makes them more valuable?)>>

JNJ

I have owned this one for decades. I remember expressing my amazement

on the old board when the market cap of the "T" word exceeded that

of JNJ.

Well run and relatively reasonably priced it gives your portfolio some

health care exposure and makes the perfect stock for what Bob Kirby

used to call "The Coffee Can Portfolio."

Bob Kirby's daughter used to post every now and then on the old board.

I will see if I can find a famous article that Bob Kirby wrote for the

Journal of Portfolio Management many years ago and post it here.

As Charlie always says BENIGN NEGLECT.

No. of Recommendations: 6

No. of Recommendations: 3

"However, more or less entirely by coincidence, so far it's [book value] about as good a yardstick as ever."

Agreed. Berkshire's price/share, and I would argue IV/share, has tracked BV/share for 58 years, and it has continued to do so since Berkshire began repurchasing shares more or less regularly. The biggest swings in BV/share result from swings in the equity portfolio, which still makes up 50% of Berkshire's BV and IV. The equity portfolio, like the broad stock market, swings from being significantly overvalued to being significantly undervalued, and it can remain overvalued or undervalued for a decade or more. Therefore, when valuing Berkshire by BV/share we need to consider whether the equity portfolio is currently overvalued or undervalued. One way to do this is to plot the stock price versus BV/share, and to use the trendline (power law) as an estimate of IV. The trendline smoothes out the ups and down in the stock price and in the BV of the equity portfolio. The only assumption in this method is that over long periods of time the price/BV oscillates about the IV/BV, i.e., that the market is a weighing machine. The growth rate of BV does not need to be constant, and indeed it hasn't been. Neither does the growth rate of the stock price need to equal the growth rate of BV, and in fact over the last 58 years the stock price has increased somewhat faster than BV, reflecting a gradual increase in IV/BV.

At times, such as in 1981 or 1998, Berhshire's price can vary significantly from the trendline of price versus BV, but I would argue that the trendline remains a reasonable estimate of Berkshire's IV, requiring no assumptions about the future growth rate of BV or of free cash flow, and no assumptions about appropriate price multiple or discount rate. Simply plot share price versus BV/share over a sufficiently long period of time to average out the up and downs, generally 30+ years, and use the trendline (power law) as an estimate of IV. BV per share remains a very good indicator of IV per share, provided that one looks at the long term trendline of price versus BV.

No. of Recommendations: 7

"BV per share remains a very good indicator of IV per share."

If we plot Berkshire's price/share from 1965 to present (semi-log), we see, of course, that it has increased substantially, from $16/share to $459K/share. If we plot Berkshire's BV/share from 1965 to present (semi-log), we see that it has also increased substantially, from $19/share to $310K/share. If we now plot price/share versus BV/share (log-log), we get a straight line with a remarkably good fit (power law). The trendline of the plot represents a decent estimate of what the market is willing to pay for a given level of BV/share. I contend that the trendline also represents a reasonable estimate of IV. This IV estimate agrees well with IV estimates by other methods.

{kind=link}