No. of Recommendations: 1

Like Mr Tilson, I take this view:

If an observer is using a sane valuation method but is forever too optimistic,

just look at whether they're more or less optimistic than they usually were in the past.

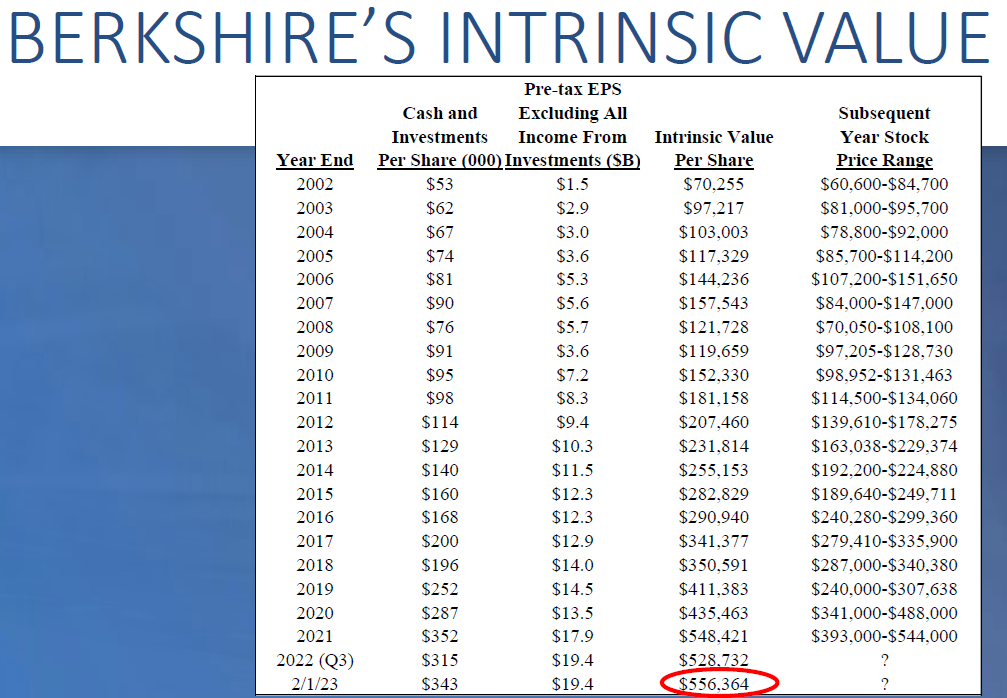

e.g., if the forecaster's past price targets ended up averaging (say) 20% too high, does he forecast more or less than 20% upside at the moment?It depends what Tilson is talking about, with his ��20% higher�� target. My take is that Tilson is just saying that, if you add investments + a constant* multiple of non-investment earnings, you get an intrinsic value 15% higher than a recent share price.

It's true that that always seems to be 10-50% higher than the share price, and in most years, the price took more than a year to reach that point:

https://assets.empirefinancialresearch.com/uploads...But constant undervaluation by the market doesn't make that wrong. After all, given Berkshire's strong share price appreciation for over 50 years, you can't really conclude that the intrinsic value wasn't there, only that the market never quite catches up to the intrinsic value. Just because you can always get it at a discount doesn't mean that it's not a discount!

You make a good point that the relative discount probably is useful in gauging future returns - for instance, if the average discount has been 25% or so, the current 15% discount should mean that we should expect a little less return from today's price than has been typical over the last 20 years. That may still be better than available alternatives, and since the broad market remains frothy in my view, and Berkshire tends to outperform when the market goes down, I like the current share price; plus I can't help thinking tomorrow's report will be pretty impressive, so I just went from an 11% position to 12%...

dtb

*He has changed the multiple from time to time: sometimes 10, sometimes 11, sometimes 12. And who knows what it should be? I would prefer a simpler calculation with no assumption about what the multiple should be - just back out the investments and calculate the multiple of operating earnings for the non-investment side; ok, adding in a number for long-term average underwriting profits, like 1% of premiums written (CR=99%)' Or use look- through earnings (plus an assumed average underwriting gain), even better'

But I assume that Tilson has at least used a constant multiple in the table I linked to.

{kind=link}