Stocks A to Z / Stocks B / Berkshire Hathaway (BRK.A) ❤

No. of Recommendations: 4

With all the chatter about Berkshire�s huge Apple investment - and the stellar returns - and the �complaint� that there are no more elephants to bag in the private equity world, �why not revert to the stock market?�

OK, OK, it�s overvalued, something which has been true for what, the last decade? The market doesn�t suffer the problem of �not big enough to move the needle�, as the Apple investment demonstrates. It can absorb endless amounts of cash. It can, if you like, pay regular dividends. You get to choose your management, at least to some degree. The financials are generally available and for a firm the size of Berkshire a little personal handholding is not out of the question.

Yes, I understand that a 5-6% risk free return on today�s cash is decent, but that�s only been true for the past two years or so. The market has green sitting there for, well, ever, and some parts of it has produced returns even better than buying down Berkshire stock.

Warren was once quite comfortable in this field. Why not so much anymore?

No. of Recommendations: 3

�why not revert to the stock market?�

If you mean buy S&P 500 or a total market indexed ETF, I would suggest repurchasing shares at current prices would be a better move. It may not be as cheap as it was a year or so ago, but I would argue still better value than the S&P 500.

No. of Recommendations: 2

why not revert to the stock market..... Warren was once quite comfortable in this field. Why not so much anymore?

Mhm, maybe because of this?

OK, it�s overvalued, something which has been true for what, the last decade?

Together with "If it's too good to be true then it's probably not true" and "As higher the climb as deeper the fall"?

No. of Recommendations: 0

If you mean buy S&P 500 or a total market indexed ETF, I would suggest repurchasing shares at current prices would be a better move. It may not be as cheap as it was a year or so ago, but I would argue still better value than the S&P 500.

I am unsure how buybacks affect future returns. Is there an equation that shows the long term expected value of buying back shares? If I invest in SPY, an assumption could be made that it will return say inflation plus say 5% forever. What is the expected future return to the shareholder for a buyback of BRK? I understand it lifts the current stock price, but does it affect the future stock price compared to not doing a buyback?

Aussi

No. of Recommendations: 5

"Warren was once quite comfortable in this field. Why not so much anymore?"

I suspect it's that he agrees with you that the market was overvalued ten year ago, and five years ago, and now. The whole business of buying "wonderful businesses at fair prices" is holding him back.

And, even with that said, buying securities is Todd & Ted's whole job description. So it's not as if BRK is neglecting the market. It's just too overpriced for needle-moving stuff, in Buffett's opinion.

/hypothesis

--sutton

No. of Recommendations: 5

Goofy,

While the following may upset those who view Buffett as being extremely rational in all things, I suspect there's a little ego involved. Sort of like declaring a dividend admits I can't find a home for all the money anymore would do.

I think Warren really believes there will come another major market opportunity to deploy cash in his remaining lifetime. And he wants to be prepared to take advantage of it.

He's a competitive guy beyond his public image.

And I do think he's avoiding some existing market opportunities in favor of retaining future flexibility. Such investments would probably go down with the market just at the time he wants the cash for other uses. Current interest rates reduce the cost of doing so.

I like BRK buybacks as an alternate. But market volumes limit the amount that can be deployed together with IV constraints.

Just an opinion.

No. of Recommendations: 1

Think of buying 50% of the company�s stock back in a Dutch auction. The price might settle at a premium of 10% or so. Use most of the cash and borrow the rest. Pay off the debt in fifteen years or less. The future earnings per share would be double current earnings with no earnings growth, could be quadruple current earnings with small growth.

Jk

No. of Recommendations: 44

I suspect it's that he agrees with you that the market was overvalued ten year ago, and five years ago, and now. The valuation of the S&P500 has varied enormously over the last 20 years, and it is now as highly priced as it was in the year 2000 - it has, with a very broad brush stroke, followed a U shape with the overvaluation - with large cap stocks expensive in 2000 and 2022, and cheap in 2010.

I wouldn't compare the price to 12-month earnings, with the margins changing so much from year to year (in April 2009 firms had almost no earnings in aggregate) but comparing

price to book value over time is a good proxy for rate of change of value. Book value isn't usually insightful when looking at individual companies but when viewing the market as a whole, it is very good because it is less sensitive to start and end points than the 10 year average earnings (CAPE) which his more commonly referred to by value investors.

Here is the price to book for the S&P500 the last 10 years:

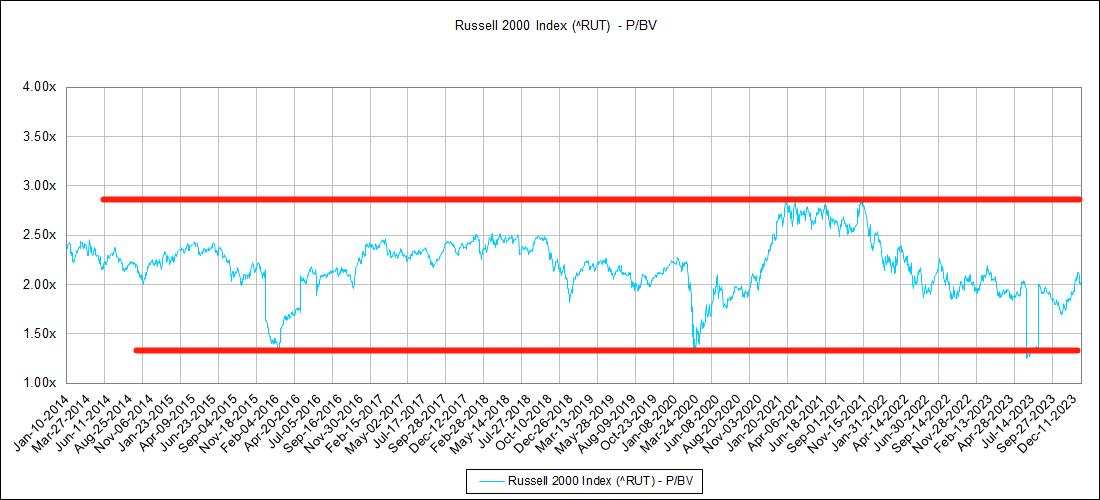

https://www.multpl.com/s-p-500-price-to-bookThat's for the S&P500 - which is what matters to Buffett as he is looking for enormous firms. However for you and me, we should not necessarily be so worried. If we take the Russell 2000 - the 2000 smaller firms within the largest 3000 firms - then right now the valuations are fairly unchanged between now and 10 years ago. Buying now is not unlike buying in 2014 for this universe of smaller firms:

https://ussnsimg.moomoo.com/feed_image/77777017/aa...If you want to look at earnings of these small caps, you must take into account the margins. The small cap margins are, as it happens, only a little elevated right now, and the present PE ratio of small caps is well below the historical average (~14x now, versus ~17x average 1999-2024, see figure 2 of link below). So the price to sales is pretty much average right now - and that will surprise a lot of people looking at the market today in 2024. In the data below, note the low PE of the S&P600 (small caps, similar to the Russell 2000) in figure 9, and then scroll up to figure 5 to check the margins - the margins are not so highly elevated (compared to the margins for the S&P500 which are greatly elevated, and what is worse, the S&P500 P/E ratio is

also high).

https://yardeni.com/charts/sp-600/If you like index investing, you can access the smaller cap stocks by purchasing IJR. This covers the same universe of small caps in the so-called S&P600, except that the S&P600 ads an extra filter that requires stocks to be profitable in the last quarter and the last year. This filter is effective. If you want to track exactly the S&P600 (including the value filter) then you can access that by purchasing

IJS instead of IJR.

Now, over the last even 20 years IJS and IJR had identical performances, however if you go back further in history beyond 30 years, adding the value filter greatly helped the performance of small cap stocks, so IJS is likely to outperform IJR over the next 20 years. Furthermore, IJS (tracking the S&P600) is almost certain to outperform the S&P500 over the next 20 years because (1) its rate of intrinsic value increase as historically been higher than the S&P500 - for example revenue per share + dividends of the S&P600 rose 10% per year the last 20 years, versus merely 7% for the S&P500, and (2) we are starting from a lower valuation with the S&P600 if starting today, so the already considerable outperformance is amplified a little more also from that.

Buffett recommends the S&P500, however the starting point

really matters even over 20 years (look at the return of the S&P500 from 2000 to 2020 and compare it to the return if starting just 5 years earlier or 5 years later - there is a very large difference).

You can alternatively avoid the expensive mega caps also with an equal weight index such as the RSP (this is really the large caps equal weighted, but that removes exposure to the mega caps which is where the overvaluation is right now).

Some of the mega cap firms are going to be go on to be investments from today, I'm sure, so it is a mixed picture, but being exposed to all of them via the S&P500 is likely to have subpar long-term returns. Almost every year there was a concept of "invincible" companies, only with the zeitgeist changing and each time the previous "invincible" turning out to be largely transient. We even revise our own memories about what we believ

ed in the past to be more consistent with the present, leaving us persistently overconfident.

( I did investigate the effect of

combining small cap value (S&P600) with equal weighting: Given that both equal weighting outperforms, and the S&P600 small cap (but cap weighted) outperforms, then why not get the best of both worlds? Well, in backtesting this idea it turns out that equal weighting the S&P600 offered no improvement long-term to the S&P600 itself. )

So from today, 2024, until 2044 (yes I'll keep Shrewd'm here), check back on this post and compare the total return of RSP (large cap equal weight), IJS (small cap with value filter), and SPY (large caps with emphasis to mega caps). I imagine RSP and IJS will be similar, but they will be both better investments than SPY. I'm optimistic as many are about the moats of the present mega caps, but I also like to sometimes read the finance section of newspapers from the distant past (1920, 1940, 1960, 1980, 2000, etc) for entertainment, noting that there was always a concept of each era being unique and the new invincible firms being more reliable than anything in the past, and going on to restructure and/or dwindle.

- Manlobbi

No. of Recommendations: 4

I have used VBR (Vanguard Small Cap Value ETF) for my small cap holding. As is usually the case with Vanguard products VBR has a smaller expense ratio 7bp vs 18 bp for IJS.

The performance has tracked each other very closely. VBR has outperformed over 5 years while IJS has a slight edge over 20 years.

https://www.morningstar.com/etfs/arcx/vbr/chart

No. of Recommendations: 2

If BRK management doesn't feel they can generate a return above the SP500 they should just return the money to shareholders, either through accelerated buy backs and/or a dividend. Buying the SPY is super easy and investors should want more from an active manager.

I always thought the special nature of BRK wasn't just the stock picking but the access to 'special' investments that are not typically offered to average investors. It would seem that these opportunities are dwindling and no longer material given the size of BRKs operations.

tecmo

...

No. of Recommendations: 1

This is a good question. It appears that Mr. Buffett does care about the size of his canvas and is averse to shrinking it, unless it cannot be justified at all by seriously hurting performance.

This view receives support in the fact that he resisted buying back Berkshire stock for a long, long time, despite repeated calls for it, and even when the shares traded closer to book value than now. At that time, I recall being puzzled by his behavior, given that he was a huge proponent of buying back stock when it trades below intrinsic value and actually pushed many companies in which he had invested to do so (including The Washington Post).

Even in recent years, many feel that he could have bought back larger amounts of Berkshire stock.

Although he did return money to the investors in the Buffett Partnership in 1969 when he could not find good good deals, it may be that, at least in some respects, he views those partners differently than Berkshire shareholders, despite statements that both groups are his "partners." For one, he knew most of those partners personally and would also invite them to his house during Christmas (per Alice Schroeder and Roger Loweinstein). However, most of Berkshire shareholders are nameless and faceless to him.

Just my 2 cents.

No. of Recommendations: 3

All that said, personally, I am glad that the option to invest in Berkshire exists. For me, the primary reason for investing in Berkshire vs. the S&P 500 is that the latter has traded at nosebleed valuation levels for the bulk of the last decade or two. Even if Berkshire's intrinsic value growth is similar to that of the S&P 500, I will continue to invest in it as long as it is more reasonably valued.

No. of Recommendations: 3

Somehow the answer to my question has devolved to �which ETF� (or other index fund) should he buy, which is the farthest thing from what I meant.

Surely there are wonderful individual stocks to be had somewhere ? No? Berkshire bought a crap-ton of Apple, even as it seemed �over-valued� at the time. Turns out it wasn�t, and it winds up being �a great business bought at a fair price.�

Is there not another one or two or three on the long list of companies which are publicly traded? So not in tech (OK, I get it). Not in pharma? Not in home building, construction, or finance? Nothing in consumer staples? Basic materials? Telecom? Utilities? Nothing in foreign markets?

I am not suggesting throwing as much at the top choices as they did at Apple. I�m asking �cash�? Sure, we all get there has to be ammunition for the big game hunt (which may never come again) and for insurance payouts, but �cash�? It�s an ungodly hoard, isn�t it?

No. of Recommendations: 0

If you like index investing, you can access the smaller cap stocks by purchasing IJR. And if you want small cap GROWTH investing, you can access that in IJ

T. Which has outperformed small caps (and MI screens, cough) for some time.

https://stockcharts.com/sc3/ui/?s=IJT%3AIJRFC

No. of Recommendations: 3

"If you like index investing, you can access the smaller cap stocks by purchasing IJR."

And if you want small cap GROWTH investing, you can access that in IJT. Which has outperformed small caps (and MI screens, cough) for some time.Portfolio Visualizer says they have almost the same returns. (Aug 2000 - Apr 2024)

IJR 9.23%� iShares Core S&P Small-Cap ETF

IJT 8.90%� iShares S&P Small-Cap 600 Growth ETF

IJS 9.13%� iShares S&P Small-Cap 600 Value ETF

SPY 7.33%� SPDR S&P 500 ETF Trust

https://www.portfoliovisualizer.com/backtest-portf...Although, since Jan 2009 SPY is best.

Also since Jan 2014, SPY beat the snot out of the others.

No. of Recommendations: 0

� Now, over the last even 20 years IJS and IJR had identical performances, however if you go back further in history beyond 30 years, adding the value filter greatly helped the performance of small cap stocks, so IJS is likely to outperform IJR over the next 20 years. �

If you like IJS you might want to also look at AVUV

https://www.etf.com/tools/etf-comparison/IJS-vs-AV...Disclosure - I do own a bit of AVUV. It�s done well and looks cheap. Uses value and profitability.

No. of Recommendations: 0

SLYV has outperformed IJS

No. of Recommendations: 32

I am unsure how buybacks affect future returns. Is there an equation that shows the long term expected value of buying back shares?

A buyback done at fair value does not change the value of the continuing shares at all.

Any buyback done above fair value reduces the value of a continuing share.

Any buyback done below fair value increases the value of a continuing share.

So much, so obvious: it's the same with buying any other stock. Bad if you overpay, good if you underpay.

So, simple math:

If a company buys back 15% of its stock at at 20% discount to fair value, the value of each continuing share rises around 20%*15% = 3%.

That's why a few billion spend on buybacks at modest discounts to fair value is not really as big a deal as many people make it out to be.

It's a little bit more nuanced when you consider that sometimes a buyback is the best available idea. Buying in shares at fair value doesn't really do anything by itself, but it's very much better than overpaying for an acquisition or branching out into a line of business with poor economics. Often it is the best of a lot of not really great alternatives.

The other thing about buybacks is this: say it's a really good company, with great capital allocation skills and a high return on incrementally allocated capital. You want to own lots of it, and buybacks (not above fair value) make tremendous sense. You want to buy as much as you can, and so does management.

But as the price paid rises, not only does each buyback make less sense because it's more expensive, but it also makes each buyback worth less because it is now a worse quality business: their capital allocation is not as good, and their return on incrementally allocated capital is worse. So there is a weird counteracting effect going on: the more buybacks you do (i.e., the less discerning you are about the price at which you buy), the less the business is worth at any given price because it's not as good at capital allocation.

If a great business only does buybacks when the shares are REALLY cheap, it's a great firm so you want them to do tons of buybacks.

But if they do those more buybacks when the shares aren't so cheap, it isn't as good a firm, so you want them to do fewer buybacks because the firm isn't as attractive at any given price...and round and round. What the wise man does at the start, the fool does in the end.

This touches on why it interests me very much that Berkshire has been doing buybacks at considerably higher levels lately. Not because I think it's a worse firm as a result per the reasoning above, but because Mr Buffett clearly *doesn't* think it's a worse firm. Yet valuations of those buybacks seems quite high, not just on simple book, but on other fancier value metrics like multiples of operating earnings or look through earnings. I read into this fact that Mr Buffett thinks the serious weakness in operating earnings in the last few years, especially in the utilities, is transient. I would say that the buybacks at recent levels make sense only if the trajectory of business value (per unit of assets or sales) returns to the old trend. As approximated by trend price/sales within the utilities and rails divisions. i.e., net margin reversion to old norms.

I think he is pretty sure it's going to get fixed.

Jim

No. of Recommendations: 23

Warren was once quite comfortable in this field. Why not so much anymore?

Because real bond yields are low.

Considering that:

(a) what we call "cash" is only a shorthand for the short end of the entire fixed income portfolio, and that

(b) the fixed income portfolio (including cash) isn't any bigger than historically normal as a fraction of the assets of the company or as a fraction,

...the conclusion is that the cash pile isn't particularly big, and won't be even at $200 billion, because there is almost nothing in the way of long term paper.

As the cash pile isn't a particularly big allocation, there is no reason to bemoan the fact that it hasn't yet been put to work or search for reasons that it hasn't been.

The only thing that happened is that the fixed income portfolio has been moved firmly towards the short end of the curve. Fewer holdings with durations over 12 months, more with durations 3-12 months. This is the reason I give the answer "because bond yields are low" above.

Cash + fixed income as percent of investments per share at end Q1 = 36%.

It was a that high or higher at every single year end from 1999 to 2019 inclusive, and averaged 48% in that stretch. We are 1/4 underweight fixed income (including "cash"), in that sense.

And the flip side: listed equities as a percent of the investments per share is much higher than the old average number (post Gen Re): much more money is currently at work in the markets than the historical norm, not less.

It's easy to forget how much bigger the company is now. There was a time that $150bn would have been an outrageous pile, but no longer.

Jim

No. of Recommendations: 7

...the conclusion is that the cash pile isn't particularly big, and won't be even at $200 billion, because there is almost nothing in the way of long term paper.

As the cash pile isn't a particularly big allocation, there is no reason to bemoan the fact that it hasn't yet been put to work or search for reasons that it hasn't been.

Another way of looking at this:

CNBC 2/24/20 WARREN BUFFETT: We own-- if you think about it, we�re 80-some-percent in equities. We may show $230 or $240 billion in equities, and that looks like we�re, against our market cap, we�re 40%. But we own 100% of these other businesses. Those are equities, too. I mean, we own a railroad. And we-- we own insurance companies. And those are-- those are equities. So, we�re about 80% in-- roughly in equities and about 20% in cash.

Taking 1.55x book as a proxy for IV:

Year (Cash + Fixed)/ IV

2010 28%

2011 25%

2012 25%

2013 21%

2014 23%

2015 22%

2016 22%

2017 23%

2018 24%

2019 22%

2020 23%

2021 20%

2022 20%

2023 22%

2024-1 23%

The current amount of cash isn't particularly high compared to IV.

No. of Recommendations: 1

"I am unsure how buybacks affect future returns. Is there an equation that shows the long term expected value of buying back shares?

A buyback done at fair value does not change the value of the continuing shares at all.

Any buyback done above fair value reduces the value of a continuing share.

Any buyback done below fair value increases the value of a continuing share.

So much, so obvious: it's the same with buying any other stock. Bad if you overpay, good if you underpay."

Jim, question for you..... In the case where a company pays a dividend do buybacks also have the added value of saving the company money because you are not paying the dividend on retired shares? Now obviously Berkshire doesn't pay a dividend but Warren has said it is highly likely we eventually will so do you think this could also be part of the reason for continuous buybacks at a fair price? Considering Berkshire shareholders tend not to sell our shares perhaps he is making it easier in the future to pay a dividend while reducing the cost by retiring shares now? Or am I overthinking this which is also entirely possible? :-)

:-)

No. of Recommendations: 16

In the case where a company pays a dividend do buybacks also have the added value of saving the company money because you are not paying the dividend on retired shares?

Not really...they are pretty separate.

Assume shares are repurchased at fair value.

Fair value for almost any firm is well approximated by some multiple of cyclically adjusted earnings, plus a constant for any "extra" cash on hand.

e.g., a company making $1 a year with $15 per share in unneeded cash might be worth (say) $30 a share, if you assume a multiple of 15 on the earnings.

Since we are assuming they are trading at fair value, the current share price is $30.

If they use the spare cash to buy back shares,

Instead of a multiple of 15 on $1 earnings and $15 spare cash, it becomes a multiple of 15 on $2 per share earnings and no spare cash...still $30 total.

The value of a share is unchanged. Other things being equal (same valuation) the share price will still be $30 despite the lower EPS. It's shocking how few CEOs seem to understand this!

In summary, for any buybacks done at a price equal to fair value for the stock:

* The cash per share goes down

* The earnings per share go up

* Those two things exactly cancel out

* The share price is therefore unchanged

* The share count, total intrinsic value of the firm, and market cap all fall. It's a smaller firm overall.

I recap all this because it clarifies your dividend question.

Because of the buybacks, the total earnings of the firm are unchanged but the EPS goes up because the total profit is divided by a smaller number of shares.

So, assuming the total dividend remains the same--(recall that "dividend" literally means "that which is to be divided", not the per share amount!)--the coupon per share will go up because the total dividend is divided by a smaller number of shares. Of course management might choose to do something else, but if they kept the same payout ratio the dividend per share would rise the same amount as the EPS.

That's what the math says. The second order thinking would address motivations. For example, in the example above management might be more inclined to pay out a dividend before the buyback than after the buyback because they have so much spare cash. It would be relatively rational for them to think about a lower payout ratio after the big buyback.

Jim

No. of Recommendations: 1

Considering that:

(a) what we call "cash" is only a shorthand for the short end of the entire fixed income portfolio, and that

(b) the fixed income portfolio (including cash) isn't any bigger than historically normal as a fraction of the assets of the company or as a fraction,

I question why looking at cash (or equivalents) as a percentage is the right way to do it. Some businesses need ready cash, the insurance business most obviously. But after those, what is all the cash for? If he�s right and there are no more elephants, it can�t be for that. If we set aside a more-than-adequate insurance reserve, what is the rest for?

Or is the market so overvalued that there are simply no opportunities there either? Really? The stock-pickers dilemma?

No. of Recommendations: 14

Some businesses need ready cash, the insurance business most obviously. But after those, what is all the cash for? If he�s right and there are no more elephants, it can�t be for that.

Why would anyone suggest they are no longer interested in elephants? They are. And that's what the cash is for, at around the same scale (relative to the size of the firm) as always.

We have been told not to expect returns that shoot the lights out. Fair enough. But they can still be above average. I think some very large investments are still in the firm's future...and at least, certainly in the firm's plans for the future.

The business model won't provide the returns it did in the past because of scale, but the business model per se isn't broken: Always have buying power at hand. Buy reliable profitable businesses at reasonable prices when the opportunity arises. Once they throw off some cash, buy more reliable profitable businesses at reasonable prices. Repeat.

Jim

No. of Recommendations: 3

Why would anyone suggest they are no longer interested in elephants? They are. And that's what the cash is for, at around the same scale (relative to the size of the firm) as always.

It�s not that they are no longer interested; Warren says (words to the effect) there are no large acquisitions available anymore of the size that would move the needle.

Arguably the Apple position is one such, but that�s not what we think of when we talk �elephants.�

No. of Recommendations: 0

"That's what the math says. The second order thinking would address motivations. For example, in the example above management might be more inclined to pay out a dividend before the buyback than after the buyback because they have so much spare cash. It would be relatively rational for them to think about a lower payout ratio after the big buyback."

I see, thank you for your detailed reply! As a long time owner in Philip Morris I was always under the assumption they were saving money on the dividend with buybacks but now, thanks to your explanation, I realise I'm as wrong as I am about my assumptions :-)

No. of Recommendations: 25

Why would anyone suggest they are no longer interested in elephants? They are. And that's what the cash is for, at around the same scale (relative to the size of the firm) as always.

...

It�s not that they are no longer interested; Warren says (words to the effect) there are no large acquisitions available anymore of the size that would move the needle.

Well, sure, but if you take out "moves the needle" then no, it's not something that he said, so it's not relevant. There are still large investment possibilities available, and investing in those takes money. Good solid investments which aren't explosively successful (a) are really good, provided there are extremely few losers among them and (b) even boring big investments need the dry powder.

The simple average one year return among S&P 500 firms in my database is 16.69%.

29.5% of those stocks had negative returns, ranging from -.19% down to -50.67%.

Now, imagine you could simply skip investing in a randomly selected 20 of the many losers, and invested equally in all the other 480 companies for the same one year period.

I tried this, and the average one year return rose to 22.1%, an increase of 5.4%.

Admittedly that's only one run, but it shows the general idea: merely avoiding a few losers, but having no particular skill at all at picking (or being able to buy) winners, will generally give rise to markedly superior results. This is a very much underappreciated advantage to Berkshire's capital allocation skills.

Jim

No. of Recommendations: 0

Now, imagine you could simply skip investing in a randomly selected 20 of the many losers, and invested equally in all the other 480 companies for the same one year period.

I tried this, and the average one year return rose to 22.1%, an increase of 5.4%.

So you got a list of 1-year losers, and then picked 20 of them randomly, and then did the test on the remaining 480 for the follow-on year?

What would be a way to select 20 or so potential losers? Low ROE and low cash? Bad relative price strength in a weak sector?

Tails

No. of Recommendations: 1

What would be a way to select 20 or so potential losers? Low ROE and low cash?

Sounds good. Also perhaps low 1yr or 5yr revenue growth.

Or maybe low ROE _and_ low 5yr rev growth

Not quite sure how would be the best way to invest in just the other 480. Maybe by buying SPY or RSP and shorting the appropriate amount of the 20?

{kind=link}