No. of Recommendations: 20

The previous update of where Brookfield is trading, relative to value, was provided here:

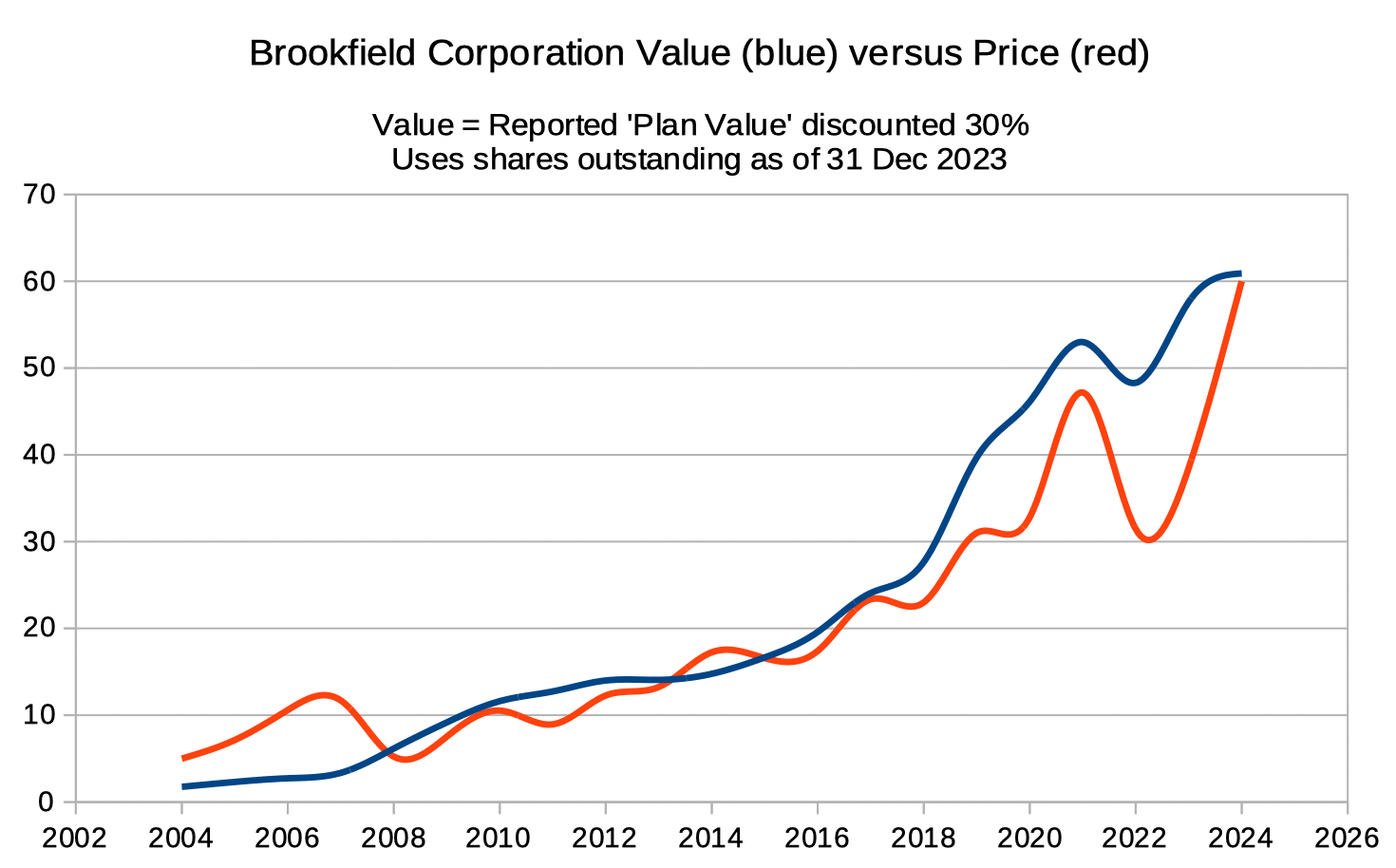

https://www.shrewdm.com/MB?pid=889218825With this new update, I am taking the reported Plan Value from September of $84, and inferring the present Plan Value by continuing the growth trend to continue for an on-trend Plan Value of $87 as of today.

The new chart is here:

http://www.shrewdm.com/investing/BN_Plan_Value_Ver...Brookfield Corporation historically traded at a 30% discount to the Plan Value and in the chart above we continue to discount the Plan Value in this way. So we are really looking at where it trades now relative to where it trades historically, rather than even facing the question of how much of the 30% discount is justified. We just assume the full discount to continue.

This week we have intersected this 30% Plan Value discount for the first time since 2015 (and briefly in 2017), having between then and now continually generally traded below it (the price at a discount greater than 30%).

To put this another way, from the quote of $60.7 today you should lower your price projection to the Plan Value rate of change itself, unlike in the recent past where we anticipated the additional bonus for the Plan Value to rise

as all as the quote/value ratio to rise along side it, resulting in superior investment returns.

Of course we can trade well above this 30% discount, and even trade at the reported Plan Value, but the assumption in this chart above is that the BN quote is more likely to deviate around the 30% Plan Value discount, than to deviate around Plan Value itself.

( For those more nerdy who are tracking the IV10/price ratio of Brookfield, if we presume Plan Value growth of 13.5% below management's expectation of 15%+ and a dividend of 0.5%, and - with where it is trading today - assume that the quote/value ratio will

not rise at all over 10 years, then we get an IV10/price ratio of 1.14^10 = 3.7. No longer a 4.0+ super investment, but still a good one for those that are patient. )

It would not surprise me at all if there are chances to pick up BN at considerably lower prices (below $50 again) for short periods over the next few years (though looking ahead 3+ years I'm not so sure, given the relentless increase in Plan Value from the nature of their semi-perpetual earnings streams, and the political lock that neoliberalism has over the world right now - turning more and more public assets into private hands). Brookfield tends to fall considerably further than the market when the S&P500 falls (BN fell 70% in the 2009 financial crisis verses the market about 50%, about 45% versus 35% during the pandemic, and 43% versus 25% in 2021-2023). Of course, timing the mood of the market is a fool's game, and if you are lightening on Brookfield now and you end up waiting 3 or more years for the next fear festival, it will be likely that you have missed out - as Plan Value would then already be 50% higher than today, and the quote unlikely to fall below $60 from that point. There is good reason that most successful investors strongly gravitate towards

staying put. All in all, just keep in mind that Brookfield is trading about where it usually does over the last 20 years, relative to its 30% discount to on-trend value, so reset your price growth expectations to lower than in recent years.

- Manlobbi

{kind=link}