Some off topic posts are okay, but please prefix them 'OT:' in the subject.

- Manlobbi

Halls of Shrewd'm / US Policy❤

No. of Recommendations: 1

No. of Recommendations: 8

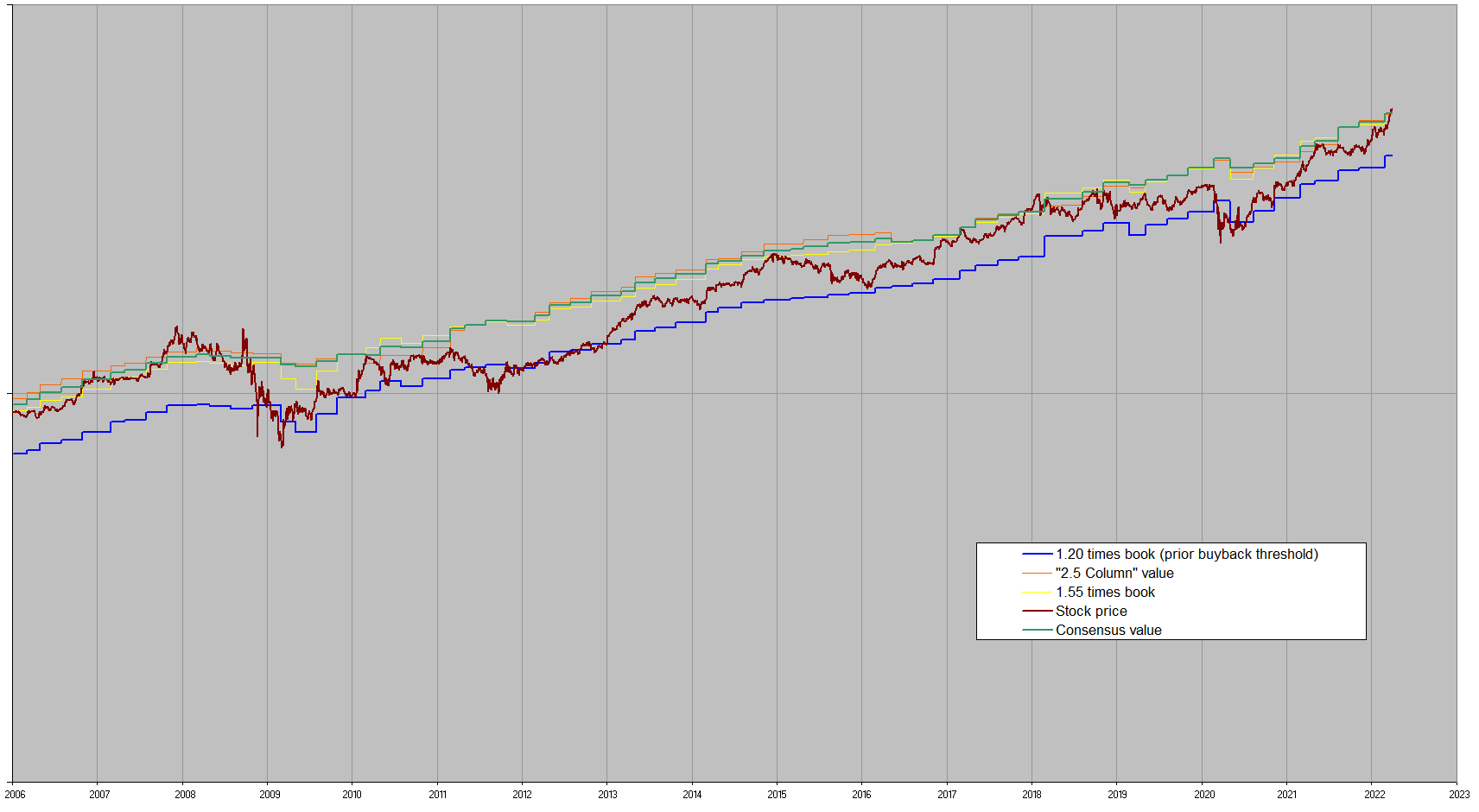

I was going to post an updated chart, but my dang ISP has blocked all ftp traffic, including the client I use to update my web site in Utah.

So I can't update my web sites, which is where I put my images...

Making some conservative guesses about what book value and estimated intrinsic value might be when the Q2 books come out,

my models suggest likely one year real returns in the range inflation plus around 4% to 5% starting from today's $350 per B.

Range from 1% to 8%, unusually wide.

This will of course climb if the as-yet-unknown 2023 business results are particularly good.

I admit to having indulged in a pinch of covered call action today. Gives me something to do.

Jim

No. of Recommendations: 2

I admit to having indulged in a pinch of covered call action today. Gives me something to do.

Yes, me too! I was going to post some questions about forward returns vs price for covered calls, but Shrewdm was giving a "505" response, so I just pulled the trigger.

The stock has run up 13% in the past six months, and it seemed unlikely that it could keep that pace for the next 18 months. Plus, I figure there's a tad of price risk, temporarily, should a C-Suite person expire in the next 18 months. After all, Warren is 92, and Charlie is 99(!).

With a midday price of $350.7/B, the Jan '25 370 Calls were selling at around $33, which meant that the breakeven was $403/B, which is 15% above today, after the nice 6-month run-up. Figured it was worth a dabble. I covered about 1/2 my position, and will reevaluate the rest after Q2 results come out. Google Fu says that will be sometime around August 4th.

Tails

No. of Recommendations: 13

The stock has run up 13% in the past six months, and it seemed unlikely that it could keep that pace for the next 18 months.

So the stock is pretty close to an all time high. In the last 926 times this has occurred since 1980, the forward 6 month return average is 12% and 1 year 26%. Of course averages cover a lot of sins as the last time it hit an all time high the 6 month return was -25% and the one year return -15% :>(

Craig

No. of Recommendations: 3

No. of Recommendations: 0

tempting to lighten up, however if i got back in at 330, its not a massive gain for me if i sold the share that are in may non taxable account. I will wait to see if it get to the the 360s-370s and possibly revaluate basis the result that should be out next week

No. of Recommendations: 0

I was kinda expecting the market to grind downtown the mean level on that chart, also given that we've had such a long bull run and are overdue a correction combined with interest wth rates.

No. of Recommendations: 4

The stock price is unchanged since one and half years ago (3/1/2022). Why is there excitement?

No. of Recommendations: 2

The stock price is unchanged since one and half years ago (3/1/2022). Why is there excitement?

It's nice to be in an uptrend at last - assuming you're not still buying, that is.

In real terms the stock price is down about 6% since 3/1/22.

No. of Recommendations: 10

The stock price is unchanged since one and half years ago (3/1/2022). Why is there excitement?

I'm not sure I'd call it excitement, at least not on my part.

Berkshire's valuation level seems to be a pinch above its modest post-crunch average, so for retired geezers like me it's not such a bad time to raise a few dollars to buy my necessities.

It's either that or sell one of the Vermeers.

Jim

No. of Recommendations: 11

It's either that or sell one of the Vermeers.

That would be the old-fashioned, honest, non-finance way.

Sell VRMR shares (fractional ownership in the Vermeer) to retail punters for more than it's worth (in total paid by all).

Keep the Vermeer yourself - "for safekeeping, you understand".

From time to time sell more shares, diluting existing ones, but at a slower rate. Your VRMR is so much better than the fiat currencies!

Also run a VRMR exchange, charge gas fees for secondary VRMR transactions.

Also offer to let VRMR shareholders deposit their VRMR shares with you - "for safekeeping, you understand". Steal - I mean, invest - some of them in your Monameda hedge fund.

Very very lucrative, but sounds like a lot of work. If you want, take a one-and-done approach. Sell VRMR NFTs to all and sundry, raise 100x the price of the painting, then burn it. Post the video on YouTube.

(To the uninitiated, yes, all of this in one form or another has been done in 2020-2023 period, though I sincerely hope not with a Vermeer.)

No. of Recommendations: 3

"Berkshire's valuation level seems to be a pinch above its modest post-crunch average"

Jim, is it possible that Berkshire's valuation in the next decade will be higher than that in the last decade because of differences in earnings attributed to the cash level (assuming that interest rates in the next decade are higher than in the last decade)?

For instance, at an interest rate of 5%, $130 billion earns $6.5 billion, which is not an insignificant amount. In the last decade, the cash position was not yielding anything close to this amount.

If this amount of $6.5 billion, very crudely, adds 12% to the look through earnings, is it likely that the valuation level increases by 12%?

I think you said that the mean P/B of Berkshire in the last decade (or roughly similar time period) was 1.35. If you add 12% to it, we get a P/B of 1.51.

Of course, one is welcome to plug in their own assumptions regarding the likely interest rates going forward, cash position of Berkshire, etc.

No. of Recommendations: 20

Jim, is it possible that Berkshire's valuation in the next decade will be higher than that in the last decade because of differences in earnings attributed to the cash level (assuming that interest rates in the next decade are higher than in the last decade)?

For instance, at an interest rate of 5%, $130 billion earns $6.5 billion, which is not an insignificant amount. In the last decade, the cash position was not yielding anything close to this amount.

In terms of valuation levels, sure, anything is possible. It might be higher. It might also be lower.

For that matter, I have no particular explanation for why valuation levels seem to have made a one-time permanent step downwards around late 2017.

The rate of growth of value (beyond inflation) remains pretty much a straight line since 1998, so it's not that.

Interest rates were pretty darned low before that, and pretty darned low after that.

And the long term index puts have expired : )

(at a substantial net final underwriting profit plus float benefit, it should be noted)

As for the interest income at Berkshire, I'm not as optimistic as some others.

Sure, we are now earning interest. Yay!

But the return on short term fixed income after taxes and inflation is actually lower, not higher, than it was before inflation and interest rates took off.

Depending somewhat on your outlook for inflation.

The recent upturn in interest rates and inflation makes things worse, not better, for Berkshire.

Keep your eye on real interest rates, with a duration in the range that Berkshire is holding. No great joy visible.

In fact, I think this is a small part of the reason that Mr Buffett has allocated a huge tranche of cash to (say) the sogo shosha and OXY. The pain of holding cash is a bit higher than it was.

Patience waiting for an elephant is a great virtue, but the amount of patience that makes sense is inversely proportional to the real after-tax cost of waiting.

But even then...taxes actually matter.

Recall that taxes are assessed on nominal returns, not real returns. 6% interest with 4% inflation is a much lower net real return than 2% interest and 0% inflation, even though they are both notionally real interest rates of 2%.

The 21% "normal" US corporate tax on the first one is 1.26%, and on the second one 0.42%, so the real after-tax return on the second one is 0.84%/year higher.

Jim

No. of Recommendations: 0

Re lower valuation multiples trending, I think given timing from 2017 it may have something to do with the succession discussion and losing the "dream team" (they can't really be replaced) indeed you could have expected a rerating to higher multiples on the back of the Apple investment, success of it and change of attitude towards technology companies.

{kind=link}